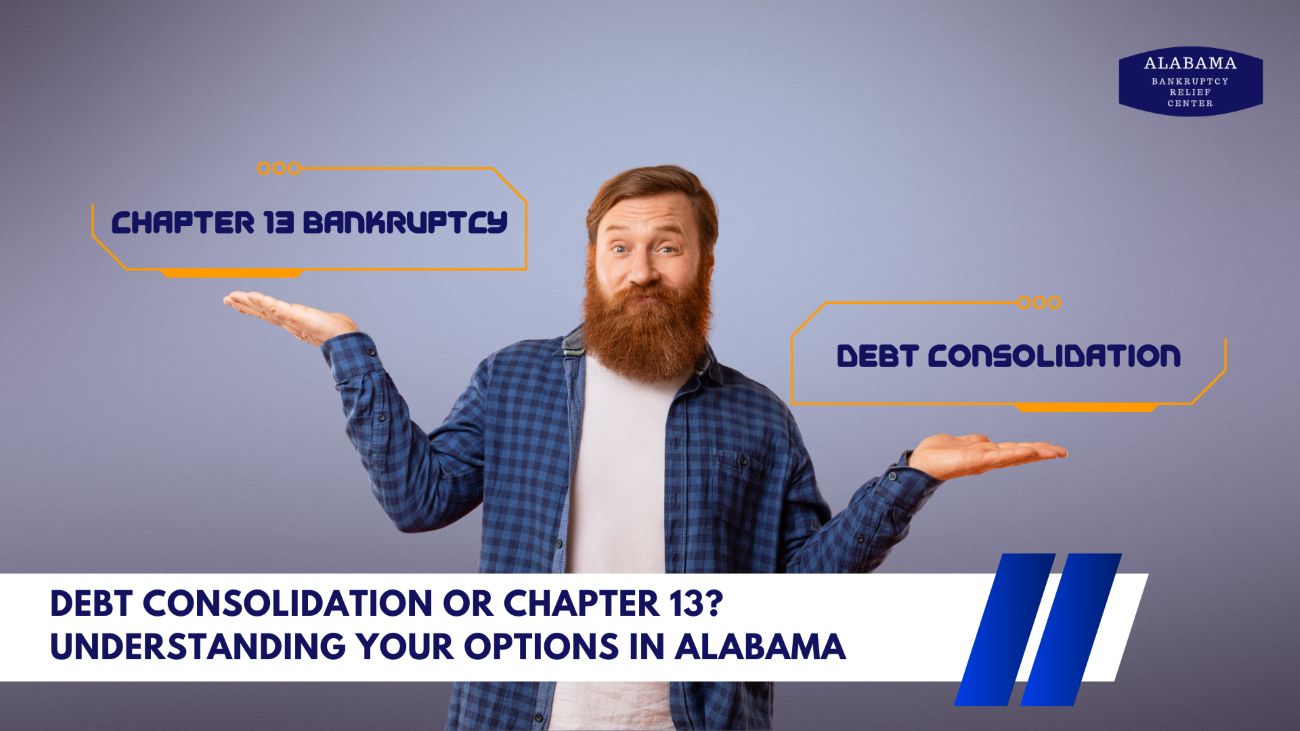

Chapter 13 vs. Debt Consolidation: What’s the Difference in Alabama?

When you’re overwhelmed by debt, it’s common to hear about debt consolidation as a possible solution. You may also come across Chapter 13 bankruptcy and wonder how it compares—or which option actually offers more protection.

While both approaches aim to help manage debt, they work very differently and can lead to very different outcomes. In this blog, we’ll break down the key differences between debt consolidation and Chapter 13 bankruptcy in Alabama, explain who’s really in control with each option, and help you understand which may better support your financial recovery.

Understanding Debt Consolidation

Debt consolidation typically involves taking out a new loan to pay off multiple existing debts, such as credit cards or personal loans. Instead of juggling several monthly payments, you make one payment to one lender.

How Debt Consolidation Works:

- You still owe 100% of your debt

- Interest may remain high, depending on your credit

- There is no court involvement

- Creditors can still:

- Sue you

- Garnish wages

- Continue collections if you miss payments

While consolidation can simplify payments, it does not reduce your debtor provide legal protection if your financial situation worsens.

Understanding Chapter 13 Bankruptcy

Chapter 13 bankruptcy is a court-supervised repayment plan designed to help individuals reorganize their debts while protecting their income and assets.

Instead of borrowing more money, Chapter 13 creates a structured plan—typically lasting 3 to 5 years—based on what you can realistically afford to pay.

Key Benefits of Chapter 13:

- Automatic stay stops collection calls, lawsuits, and garnishments

- Payments are made through a court-approved plan

- You may only repay a portion of what you owe

- No interest continues accruing on many debts

- Remaining eligible debts may be discharged at the end

Chapter 13 is governed by federal bankruptcy law, which means creditors must follow strict rules—and cannot act outside the court’s authority.

Who’s Really in Control?

This is one of the most important differences.

- Debt Consolidation:The lender controls the terms. If you fall behind, they can take legal action immediately.

- Chapter 13 Bankruptcy:You are protected by federal law. Creditors must follow the repayment plan approved by the court, giving you stability and predictability.

For many Alabama residents, that legal protection makes all the difference.

Example

Let’s say Mark, a Birmingham resident, has:

- $45,000 in credit card debt$10,000 in medical bills

- High interest rates and frequent collection calls

Mark considers debt consolidation but is only approved for a loan with high interest—and one missed payment could put him back at risk of lawsuits.

Instead, Mark files Chapter 13 bankruptcy. His collection calls stop immediately. His debts are reorganized into a manageable monthly payment based on his income. After completing his repayment plan, a portion of his remaining unsecured debt is discharged—giving him a true financial reset.

Which Option Is Right for You?

Debt consolidation may sound appealing, but it doesn’t offer the legal protection or long-term relief that many people truly need. Chapter 13 bankruptcy can provide:

- Greater protection

- More predictable payments

- Potential debt reduction

- A clearer path forward

If you’re considering debt consolidation, it’s important to understand all your options first.

At Alabama Bankruptcy Relief Center, we help individuals and families understand whether Chapter 13 bankruptcy or another solution makes the most sense for their situation.

Call us today for a free case evaluation at 205-860-7708 or schedule an evaluation to discuss your options and find a plan that protects your future—not just your payments.

Attorney Matt Davis

Attorney Matt Davis

A recognized trial lawyer and author of multiple books, Attorney Matthew Davis saw a need in the community to help people reclaim their financial freedom. He founded the Alabama Bankruptcy Relief Center with the purpose of helping the people of Alabama fulfill this mission. Read more

Find out how you can achieve financial freedom through bankruptcy.

Get your FREE book today!

Click Here

Hours

Monday-Friday 9am-5pm

Saturday-Sunday

by Appointment

Contacts

Email: help@alabamabankruptcyrelief.com

Tel: 205-440-3113

Fax: 205-564-0532

Other: 205-708-0320